How We Classify Company Stages of Evolution

How the business world refers to company stages of evolution can be, at times, a little confusing.

Funding rounds are often referred to as ‘Series A’, ‘B’, ‘C’, etc. (mainly in the US), or ‘First Round’, ‘Second Round’, etc. (in the UK). It’s second nature to think of startup investment in this way, with companies, investors, and the press all relying on these terms.

However, despite their prominence, there are issues arising from traditional life cycle labels. This is due to inconsistent definitions and increasing round sizes. What these different series and round categories actually mean can vary hugely by sector, country, or investor type.

For instance, at the time of a ‘Series C’ fundraising, a three-year-old pharmaceuticals firm may still be in pre-clinical trials, whilst a software venture may be one of the biggest emerging companies in the world.

A cross-sectoral classification system is necessary. It allows you to conduct more informed analyses, and reliably identify key trends, areas of potential, or industries that are currently underfunded. But the current system lacks nuance.

The industry needs terminology that consistently, and impartially, classifies a company’s stage of evolution — so here’s our solution.

How do we track a company's stage of evolution?

Here at Beauhurst, we monitor every company in the UK and Germany, giving a comprehensive overview of both nations’ business economy.

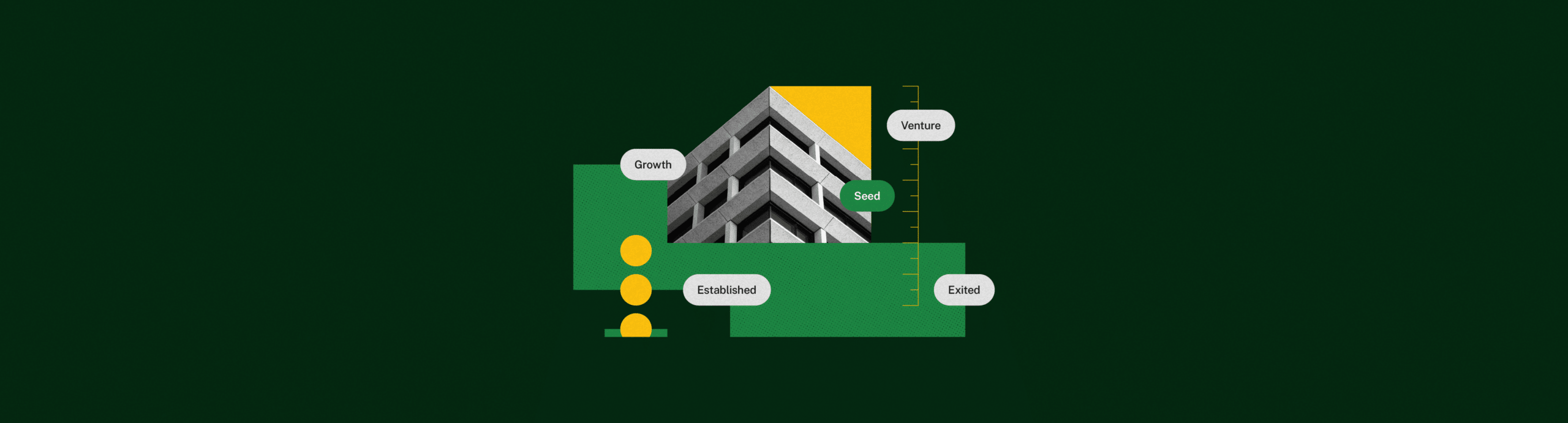

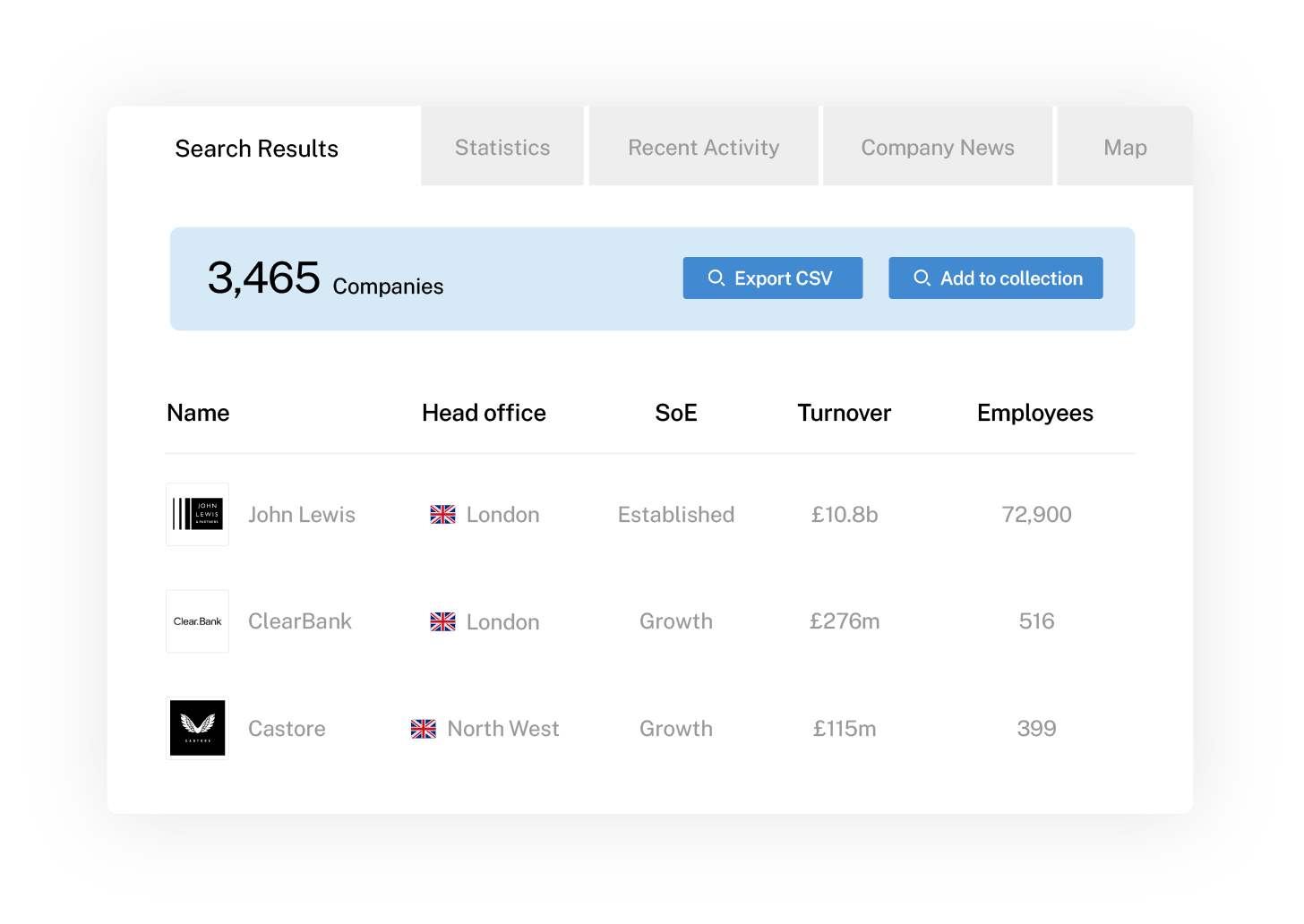

As part of this, our Data team marks relevant companies with a life cycle stage as one of: Seed, Venture, Growth, Established, Exited, Zombie, or Dead. Similarly, the fundraisings held by businesses at these stages are classified to match.

Using our methodology, while a pharma company operating at the Seed-stage and a software company operating at the Growth-stage might both self-report a Series C round, we’d classify them as Seed-stage and Growth-stage rounds.

And the Beauhurst platform gives you a comprehensive timeline, showing how companies grew to each stage and the different types of funding and support they used along the way.

Take a tour

Defining our company life cycle stages

Life cycle stages are flexible, and a Venture-stage business in one industry may be a Growth-stage company in another. Still, here’s a quick rundown of each of the stages of evolution on the Beauhurst platform — and how we use them to classify UK and German companies.

Seed

A Seed-stage company is a young startup, with low employee count, valuation, and total equity investment raised. There may still be uncertainty as to whether its product or service has an adequate market, or it may be working to gain regulatory approval. The most common sources of funding for companies at the Seed-stage of growth are grant-awarding bodies, crowdfunding platforms, and angel investors.

While most Seed investments are under £1m, the biggest Seed-stage round in 2025 was secured by Fidra Energy. The battery energy storage firm secured a £445m deal in September 2025, with EIG Partners and the UK’s National Wealth Fund participating.

Venture

Venture-stage companies have developed their business models and technology over multiple years, typically securing investment and a valuation in the millions. They’ll have strong, growing revenue figures, and may be expanding their initial product range. Venture rounds typically involve private equity and VC funds, although they may still tap into crowdfunding too.

The most valuable Venture-stage investment of 2025 was for biotech firm Isomorphic Labs, which secured £449m to fund AI research and development for building its drug design engine and advance its program into clinical development.

Growth

Usually running for more than five years, Growth-stage companies are active in multiple locations, possess substantial revenues, and boast a large and growing headcount.

They may also be profitable, have a highly valuable patented technology, or have received funding and a valuation stretching into the millions.

Funding for Growth-stage companies is likely to come from venture capital firms, corporate venture funds, asset management companies, and traditional mezzanine lenders.

In 2025, NScale secured two of the top three largest Growth-stage investments, worth a combined £982m. The UK-based neocloud develops and builds AI data centres and GPU supercluster infrastructure, and has been identified as a key growth partner for building out AI infrastructure in the UK.

Established

An Established-stage company has been trading for 15+ years, or 5-15 years with a three-year consecutive profit of £5m+ or turnover of £20m+. These businesses usually have several offices and a widely-recognised brand. Funding at this stage is often deployed by corporates, private equity firms, banks and specialist debt funds, or major international investors.

The largest investment into a company at the Established-stage of growth in 2025 was The Ardonagh Group’s £1.82b deal, with participants including the Abu Dhabi Investment Authority (IDIA).

Exited

We assign an ‘Exited’ classification when a company is absorbed by another entity and no longer operates independently, normally via acquisition or reverse takeover.

For a high-profile example, look no further than DeepMind, which was acquired by Google in 2014 for £400m. The company was subsumed into Google as Google DeepMind and is therefore no longer an independent operator.

Exited profiles are still updated, however, as shown by DeepMind’s 2016 acquisition of Imperial College London’s medtech spinout, Hark.

Listed companies are usually still tracked at the Established-stage post-IPO, as they are still functionally autonomous.

Zombie

A zombie company is our name for businesses that have been neglected for a long time or are in a troubled financial state. Whilst the company is not ‘dead’, it doesn’t appear to be operating: the company’s website/social media shows prolonged, uncharacteristic neglect, or the company’s status on Companies House is troubled (i.e. in administration, liquidation or dissolution first gazette).

A down-round is not sufficient reason for a company to be classed in the Zombie-stage — though we would assign a Risk Signal — nor is a holding company that has stopped trading, provided that its subsidiaries are still operating as normal.

Dead

See the platform for yourself

Fancy looking at the new industries classifications in action? Fill in the form below to book a meeting directly with one of our team members.

| Stages of evolution | Applicability criteria | What a typical company would look like |

|---|---|---|

|

Seed |

As a rough guideline: a youngish company with a small team, low valuation and funding received (low for its sector), uncertain product-market fit or just getting started with the process of getting regulatory approval. Funding likely to come from grant-awarding bodies, equity crowdfunding and business angels. |

• A one-year-old software company with three employees, product in private beta, £50k in funding and £200k pre-money valuation. • A three-year-old pharmaceuticals company in pre-clinical trials with £2m in funding and £4m pre-money valuation. |

|

Venture |

As a rough guideline: a company that has been around for a few years, has either got significant traction, technology or regulatory approval progression and funding received and valuation both in the millions. Funding likely to come from venture capital firms. |

• A hardware company with a first product out and some revenue. • A restaurant chain that expanded from one branch to five. |

|

Growth |

As a rough guideline: a company that has been around for 5+ years, has multiple offices or branches (often across the world), has either got substantial revenues, some profit, highly valuable technology or secured regulatory approval significant traction, technology or regulatory approval progression, funding received and valuation both in the millions. Funding likely to come from venture capital firms, corporates, asset management firms, mezzanine lenders. |

• A materials technology company with lots of patents that counted multiple governments and defence companies as clients on multi-year contracts. • A manufacturing company with factories in 5 countries, millions in revenue and some profit. |

|

Established |

As a rough guideline: a company that has been around for 15+ years, or 5-15 years with a 3 year consecutive profit of £5m+ or turnover of £20m+. It is likely to have multiple (often worldwide) offices, be a household name, and have a lot of traction. Funding received, if any, is likely to come from corporates, private equity, banks, specialist debt funds and major international funds. |

• A hundred-year-old family-owned retail company with stores in many countries, millions in revenue and profit. • A twenty-year-old software company, with large revenues and some profit. |

|

Exited |

The company has done an IPO or been acquired. (We do not consider MBOs to be exits, i.e. reasons to stop tracking companies, but rather a trigger for starting to track a company.) |

• A company that listed on AIM. • A company that was acquired by a trade buyer. |

|

zombie |

The company has met one or more of these conditions:

The company’s website and/or social media presence show prolonged neglect.

The company’s key people have all left the company and it appears to have no employees.

The company has appointed administrators or liquidators.

The company’s status in Companies House is dissolved but the company still appears to be active. |

• A company that used to update its website’s news page and/or post on social media often but has not done so for 6 months, or whose website and/or social media pages are no longer available. • A company that used to have employees on its LinkedIn profile but now has 0, and the LinkedIn profiles of all key people show them moving on from the company. • A company that has been taken to court by its creditors, or has entered voluntary liquidation or administration. • A company whose legal entity has been dissolved but appears still to be trading, perhaps only under a foreign legal entity. |

|

Dead |

The company has met one or more of these conditions:

The company has definitively ceased all activity.

The company has dissolved in Companies House with no activity.

The company, or its assets, have been acquired in a distressed deal.

The company has been at Zombie stage for a prolonged period of time.

The company has relocated its primary location outside of the UK. |

• A company that has announced on its website that “It was a fun ride but it’s over, folks”. • A company whose ultimate parent has been formally dissolved in Companies House with no signs of activity. • A company that has been acquired out of administration. • A company that has been at Zombie stage and shown no sign of activity for a minimum of 6 months. • A company whose founder has announced the opening of a new head office which is abroad. |

Track the full UK and German markets on Beauhurst

Company stages of evolution are just one dimension by which you can view UK and German companies on Beauhurst. From AI lenses, giving you instant insights into any company’s activities, through to innovation, growth, and risk signals, the Beauhurst platform offers a comprehensive view of every company across the entire economy.

Want to try Beauhurst? Take a quick online tour of the platform, or for a more bespoke platform demo, get in touch with our team.

Discover our data.

Get access to unrivalled data on the companies you need to know about, so you can approach the right leads, at the right time.

Schedule a conversation today to see all of the key features of the Beauhurst platform, as well as the depth and breadth of data available.

We’ll work with you to build a sophisticated search, returning a dynamic list of organisations that match your ideal customer profile.

Beauhurst Privacy Policy