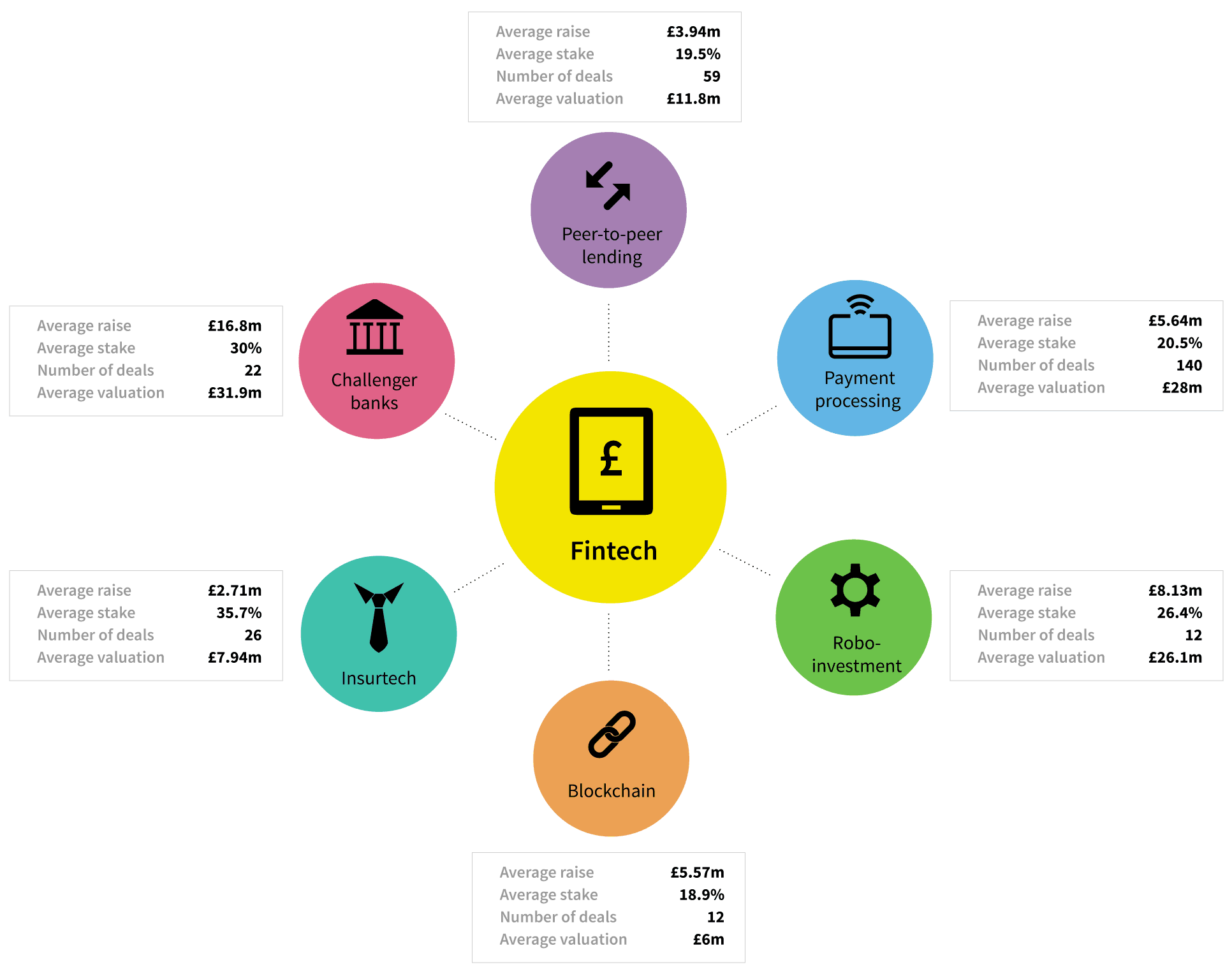

Challenger banks are fintech companies that both provide the services you’d expect of a retail bank, and aim to disrupt the current dominance of traditional retail banks. Many challenger banks offer services for small firms as well as individuals, and provide a range of traditional services (mortgages, saving, moving money) alongside more innovative features (spending breakdowns, instant transfers, simple cross-border payments).

From big names like Atom and Monzo through to relative unknowns (at the moment!) like Folio and Loot, challenger banks are one of the most exciting types of company to watch within UK fintech – just take a look at their growth over time. We’ve profiled some of the key players in the past: take a look at Atom, Tandem (twice), and Revolut, and you can find a more general overview of the sector here.

Payment processing