A classic bubble pattern is when growth is sustained by circular financing: suppliers fund customers, inflating demand that ultimately relies on fresh capital.

We’ve seen this risk discussed heavily in the US, particularly around supplier concentration and vendor financing. UK AI has a different profile. Most UK AI companies sit at the application layer, which means their dependency risk is less “stock market crash” and more platform exposure.

The biggest investors in UK infrastructure remain predominantly US-based tech giants — all of which have a very literal vested interest in AI becoming the next hypergrowth industry.

Conversely, in a hypergrowth market, the expansion is driven by businesses reinvesting their own cash profits into AI to secure measurable productivity gains.

In this scenario, demand outstrips supply, proving that the industry can scale through genuine resource scarcity rather than speculative hype. Data centre vacancies, for example, are at an all-time low of 7.6% in London.

What to watch next? Whether the UK can build its own infrastructure providers in the form of neoclouds and hyperscalers, in addition to NScale.

Indicator 4: Capital efficiency signals

Companies operating in a bubble will burn capital without a clear path to profitability, with revenue lagging far behind valuations. Hypergrowth companies exhibit growth funded by record-high free cash flow and retained earnings, rather than just debt.

Currently, AI revenue is surging across the board, but unit costs remain a significant hurdle. Unlike traditional SaaS, AI requires expensive compute for every query and so has meaningful marginal costs for additional customers.

This creates an “inference tax”, a drag on gross margins that many AI businesses can’t avoid. Now, token prices are trending down, but inference costs can trend upward as reasoning models become more sophisticated and computationally demanding.

That means the key question isn’t “is AI adoption happening?” — it clearly is. The key question is: “can AI businesses deliver value and transformation at a unit cost that supports sustainable margins?”

What to watch next? We’ll be looking at capital efficiencies and evidence of startups reducing dependency through proprietary data.

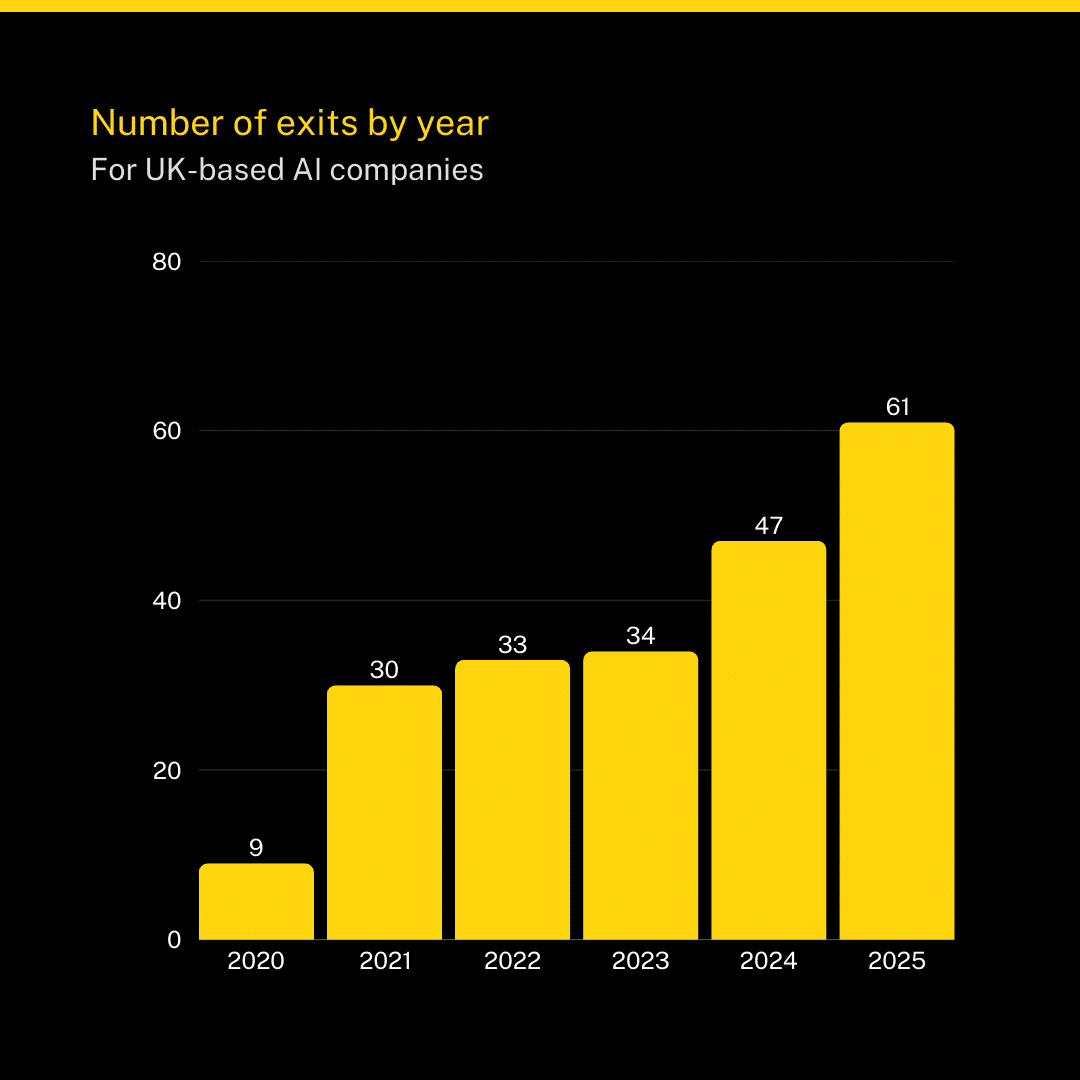

Indicator 5: Rising exit activity

A functioning market needs exits. Without liquidity, capital stays locked, and early-stage activity dries up. In the UK, exits are trending in the right direction.

The number of exits featuring AI companies rose from 9 in 2020 to 61 in 2025. That kind of increase suggests the ecosystem is producing businesses that incumbents want to acquire and that some value is being realised even as funding conditions tighten.

Most exits are still acquisitions, which is typical at this stage. But the direction matters.