The latest data on equity investment trends in the UK. We’ve analysed every publicly-announced equity fundraising in H1 2019, to spot emerging trends and patterns in the market.

See our yearly edition, The Deal, for in-depth analysis and features on key market trends.

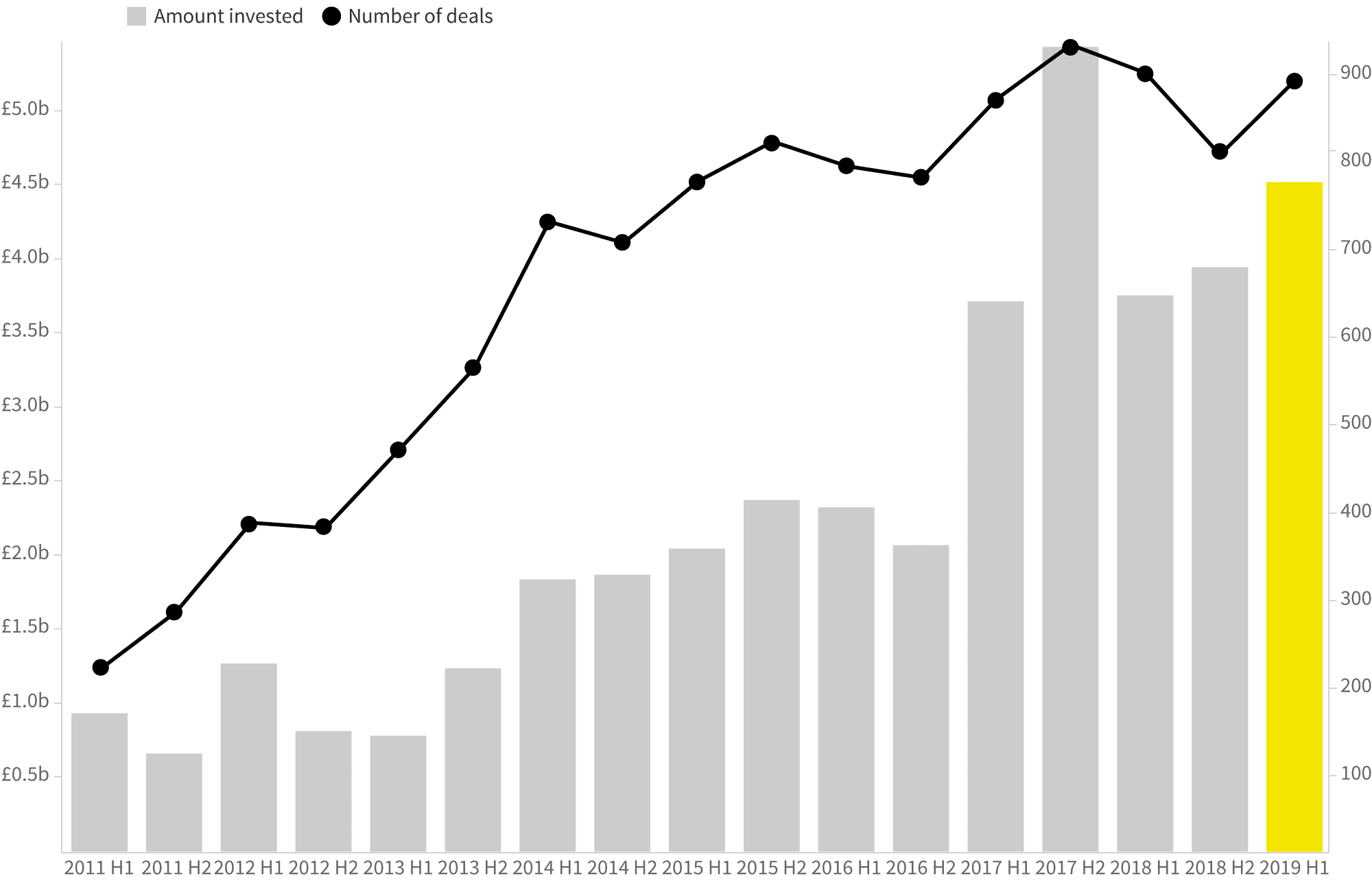

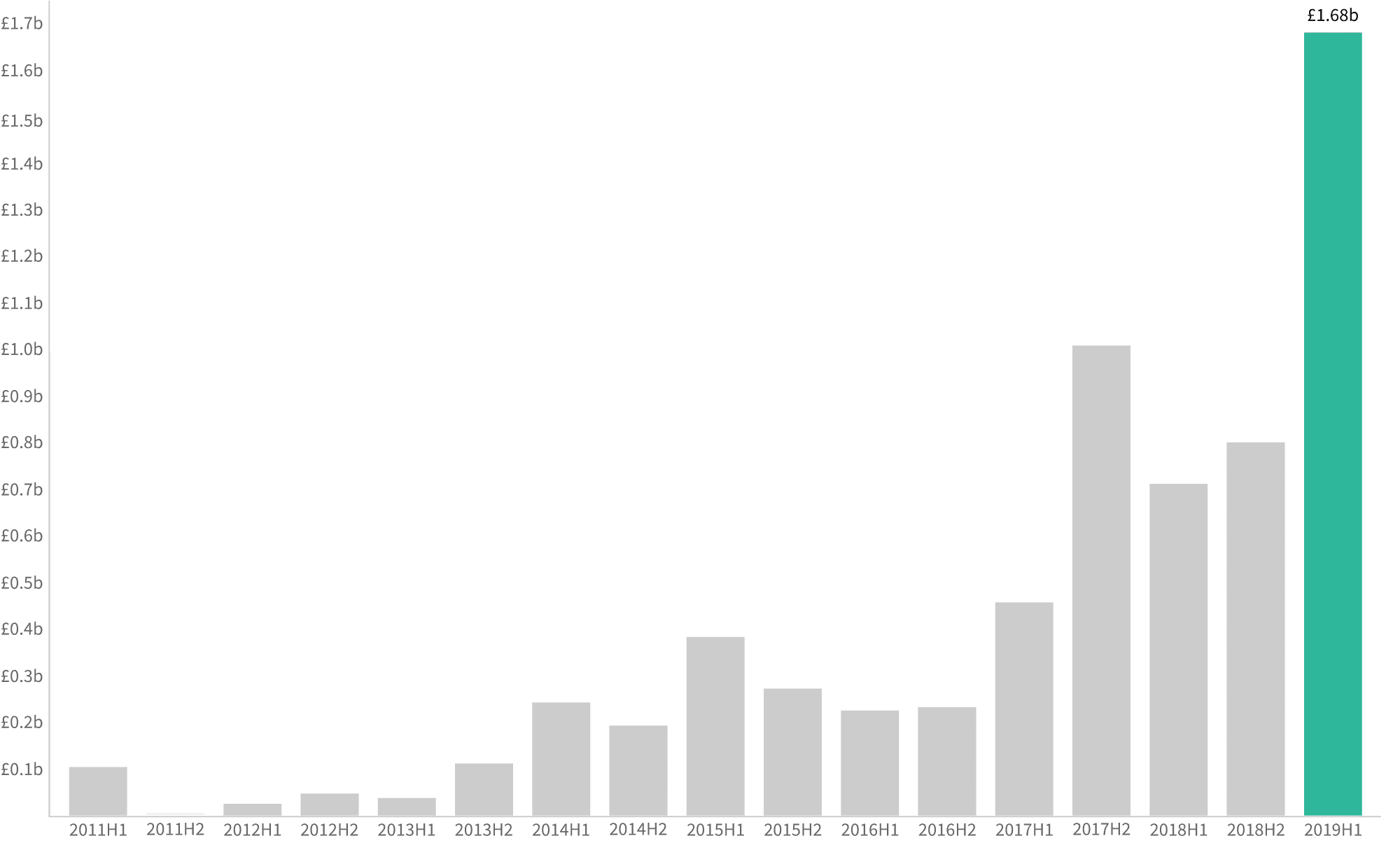

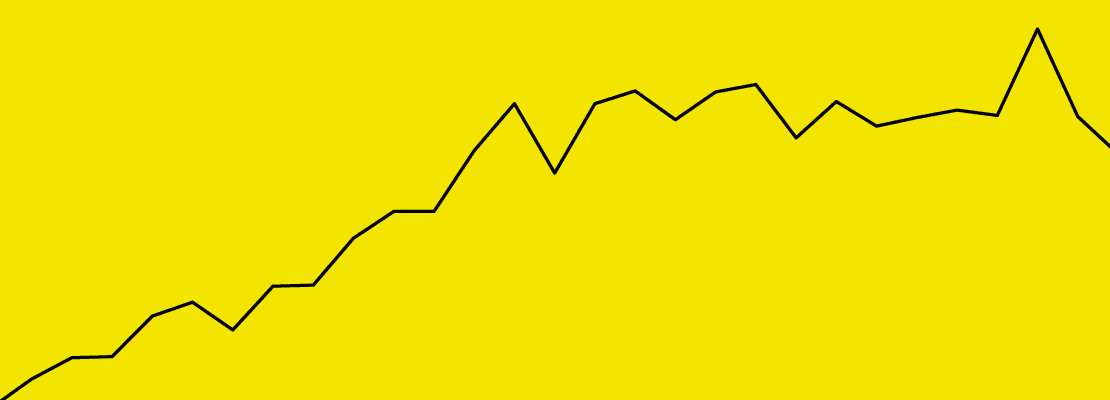

- H1 2019 was the best first half on record, with a 15% increase in the total amount of investment received by the UK’s startups and scaleups.

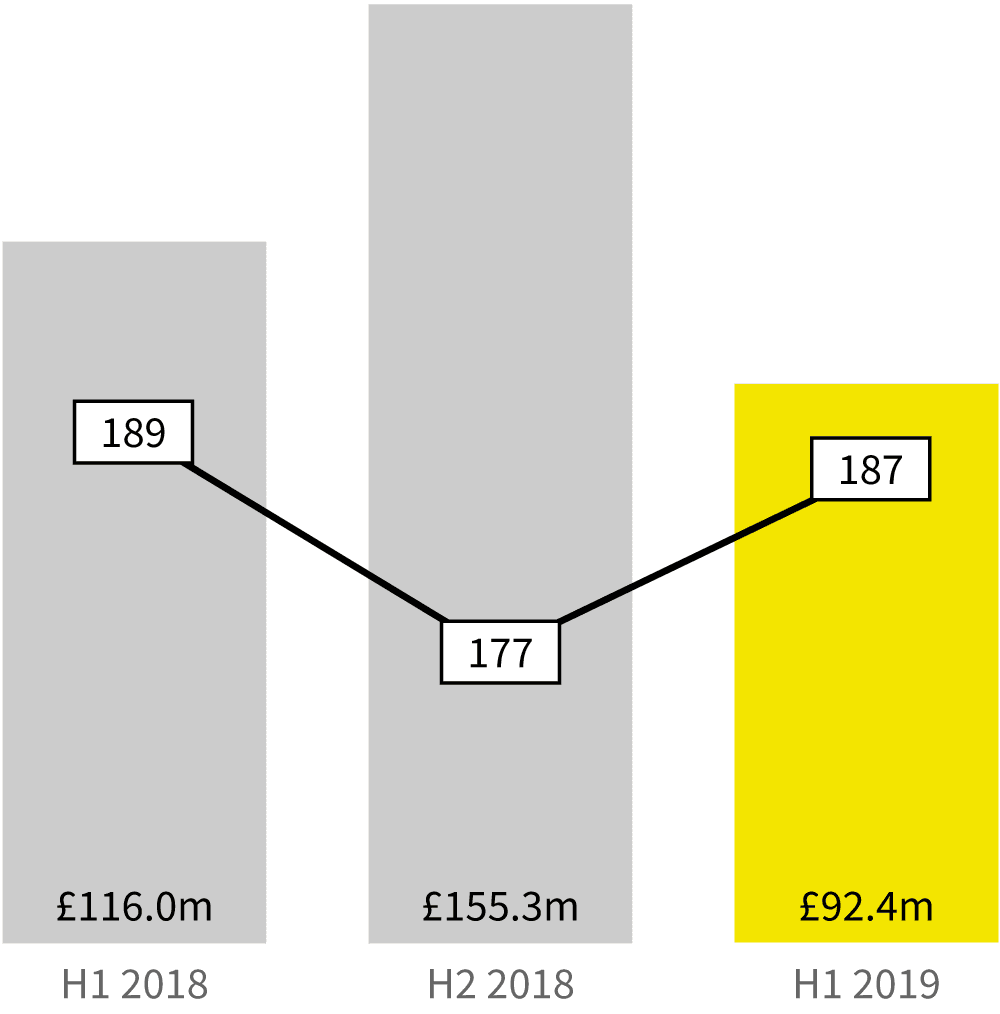

- The number of deals rose 10% since the previous half, and the majority of the increase was at the seed-stage.

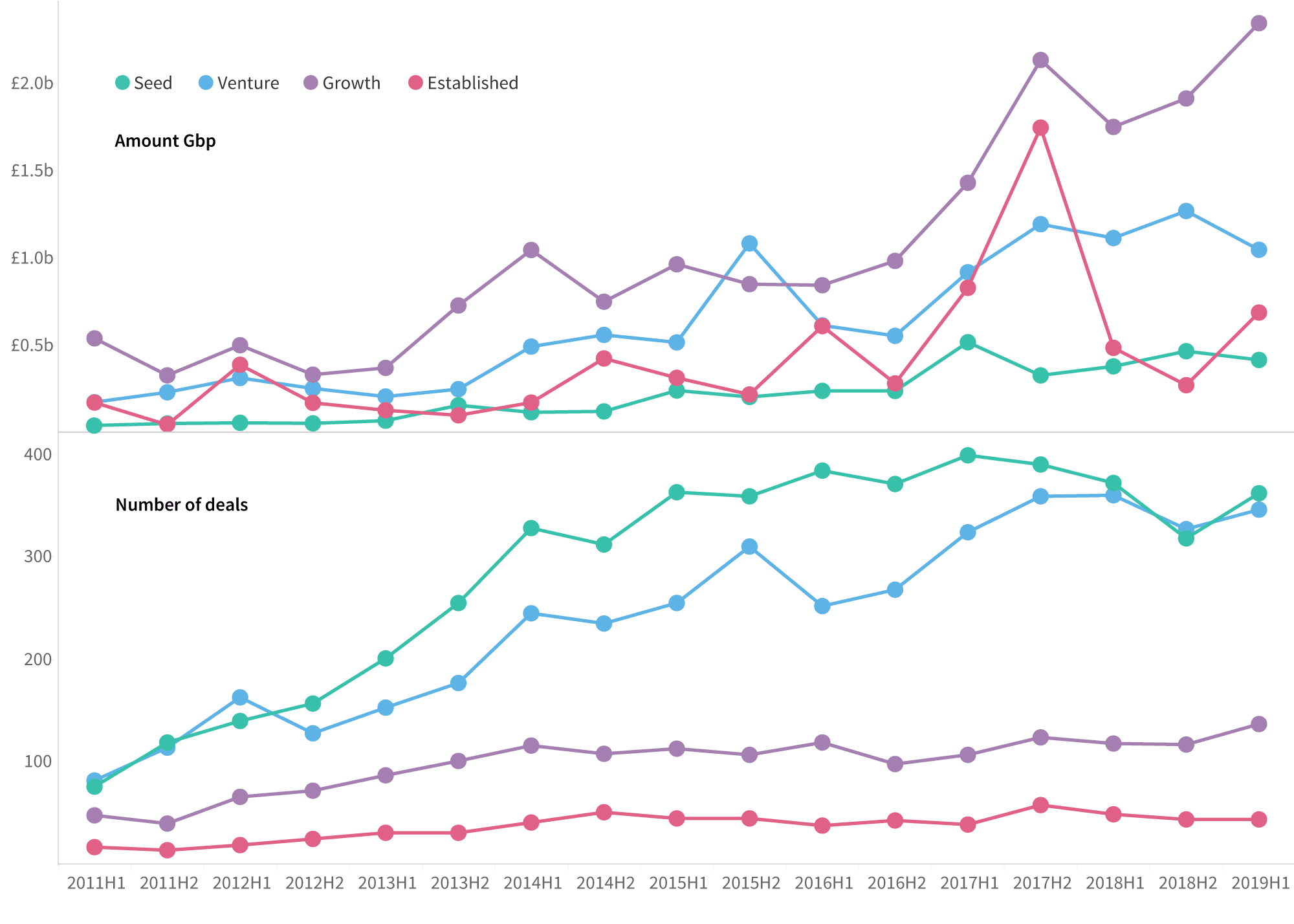

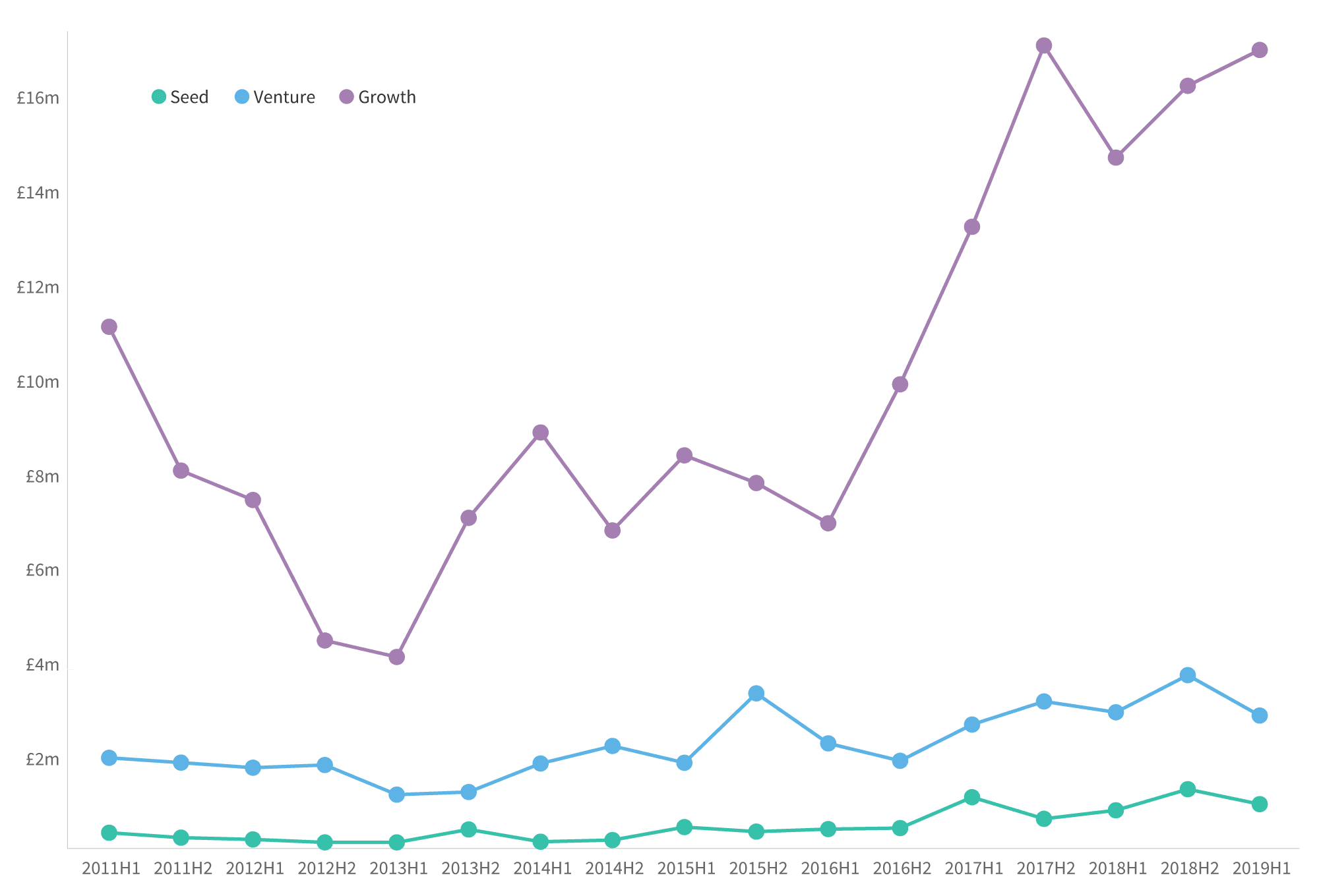

- There was also a 17% increase in the number of growth stage deals and their average size rose from £16m to £17m.

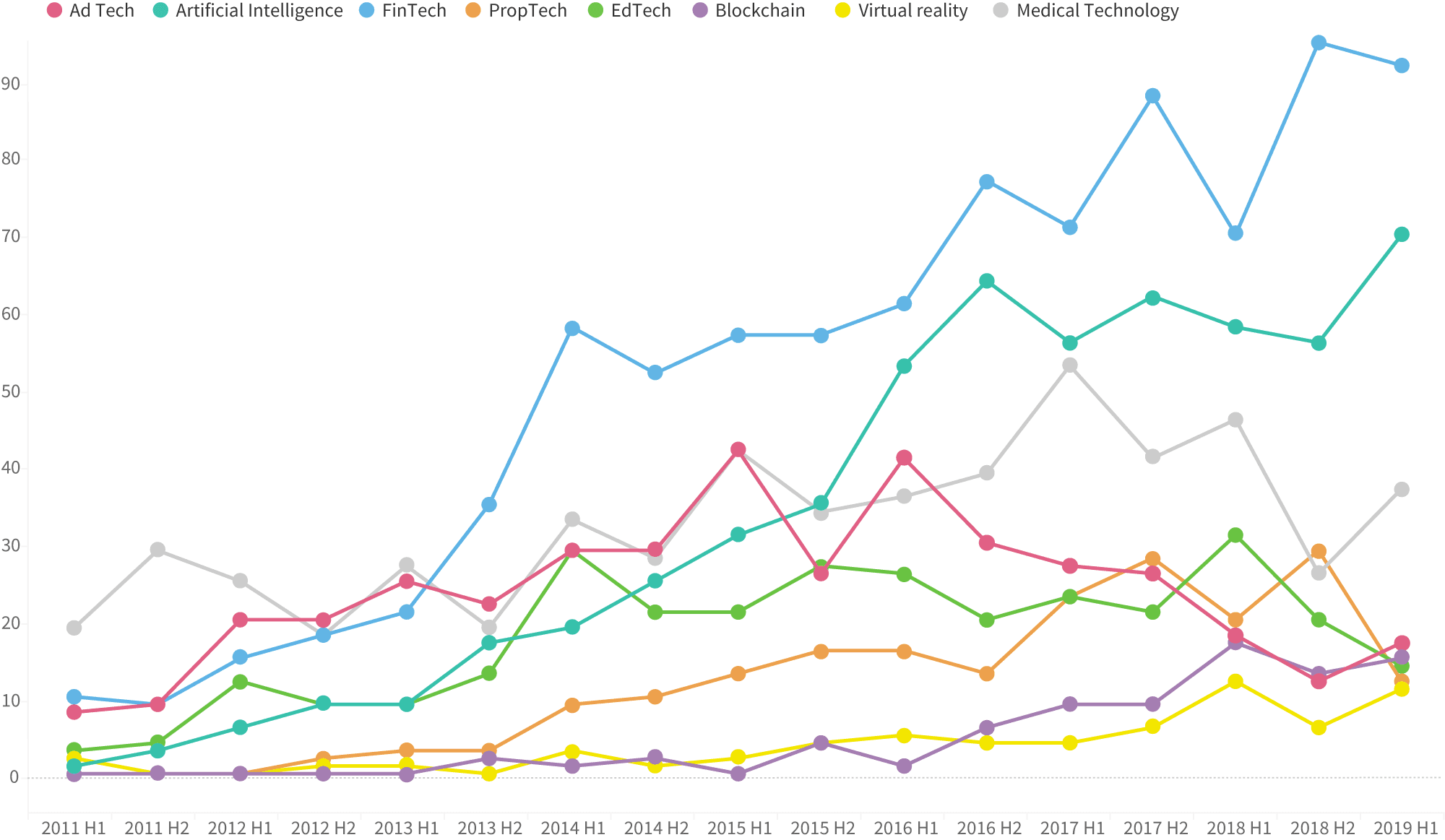

- FinTech saw more money invested than in any other half, and has already beaten figures for the whole of 2018. AI was the only sector to achieve a record number of deals.

deal numbers and amount invested