IPO vs Acquisition: How to tell if a company is about to exit

Category: Uncategorized

As we recently reported, the vast majority of startup entrepreneurs exit their businesses via an acquisition, as opposed to an initial public offering. As of June, 2019 has seen 200 acquisitions of fast-growing British companies, but only three IPOs. In a sense this makes an IPO a more exclusive, and perhaps more prestigious form of exit. That said, acquisitions may be preferred in many situations for entrepreneurs and investors looking to make a quick, less drawn out return on their money/efforts. But what can signify a company is about to exit? Since the start of 2017, there have been 47 IPOs by companies that have also fulfilled one of our fast-growing business triggers, as well as 1,759 acquisitions. This provides a reasonable sample for assessing some of the key attributes of these exit strategies.

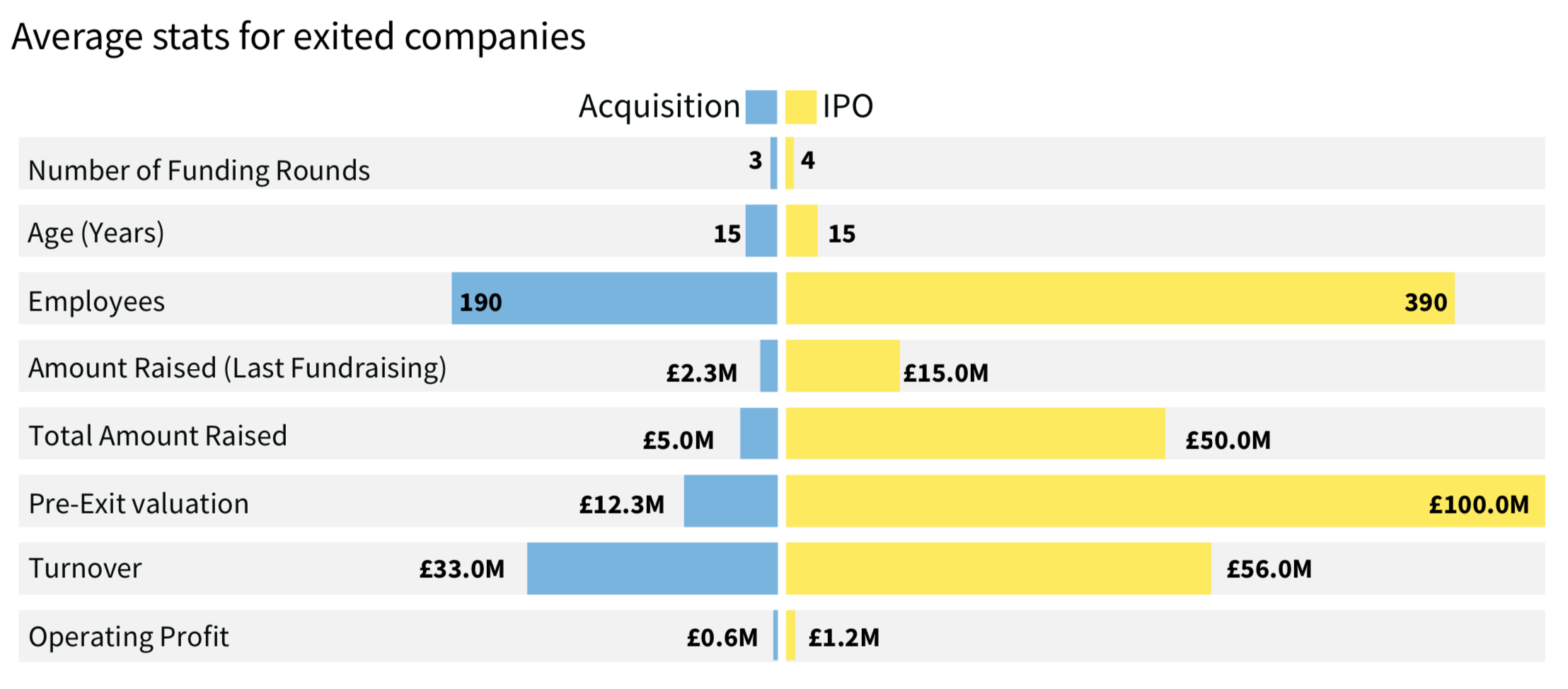

The average stats for companies prior to IPO are as follows:

Averaged stats for pre-IPO companies

| Metric | Average Value |

|---|---|

|

Funding Rounds |

4 |

|

Amount Raised (Last Funding Round) |

£15m |

|

Total Amount Raised |

£50m |

|

Pre-IPO valuation |

£100m |

|

Turnover |

£56m |

|

Operating Profit |

£1.2m |

|

Age (Years) |

15 |

|

Employees |

390 |

Note: this sample only relates to fast-growing business in the UK since 2017, so should not be extrapolated further.

Whilst there is a large amount of variation in the sample, these average values indicate the general stage of development that a company reaches before they IPO. Of course it is important to remember that the fast-growth business ecosystem is dynamic and things change quickly: for instance, our data suggests startups are taking on larger private rounds whilst putting off IPOs. The case in point would be our current cohort of unicorns, who are all opting to raise large late-stage venture rounds and enjoy the benefits of private register for longer. There are also important differences between sectors, as our recent analysis of the IPO market highlights.

Generally, if the company is already large and well-known, there will be a good deal of anticipation in the business media, and will rarely come as a surprise. The turnover and operating profit stats are particularly interesting, as they suggest the company has begun to achieve real significant sales alongside a substantial profit by the time they IPO.

Two of the biggest exits since 2017 were those of Farfetch and Funding Circle, two startups that had already received a $1b valuation. Farfetch had raised over £500m altogether, whilst Funding Circle had raised £250m. Both were under 10 years old, and their pre-IPO funding rounds came to $397m and £82m respectively. When companies start securing these amounts of venture capital funding, there will be increasing investor pressure to exit, and an IPO is most likely on the cards.

For acquisitions, the picture is slightly different:

Averaged stats for companies acquired since 2017

| Metric | Average Value |

|---|---|

|

Funding Rounds |

3 |

|

Amount Raised (Last Funding Round) |

£2.3m |

|

Total Amount Raised |

£5m |

|

Pre-IPO valuation |

£12.3m |

|

Turnover |

£33m |

|

Operating Profit |

£600k |

|

Age (Years) |

18 |

|

Employees |

190 |

Again, this sample relates to private companies that have fulfilled one of our fast-growth triggers, meaning the sample is heavily focussed on the early-stage startup and SME market.

These stats show that acquired companies tend to be smaller, less valuable and less well-funded than counterparts about to enter a public market. They’re also older, suggesting these companies have taken a slower, less capital and growth intensive pathway to commercial maturity. This matches expectations: barring large corporate mergers, acquisitions will generally be made by larger companies of smaller rivals. Perhaps the acquired company be just starting out, and in possession of some desirable technology or IP (such as Bristol spinout Ziylo, which developed molecules that can be used for treatment of diabetes). Usually, however, it will be late-stage, with the original founders or management nearing the end of their careers and looking to make an exit on their efforts.

Ziylo is particularly interesting because of its anomaly status. Whilst just four years old, the spinout was acquired in a deal that could be worth more than £600m, if certain commercial milestones are met. It was acquired by the Danish multinational pharmaceutical company Novo Nordisk, who were clearly interested in the young company’s tech – a “smart insulin” drug that could adapt itself automatically to levels of glucose in the blood.

At the other end of the spectrum are a whole host of very old companies that have been acquired since 2017. Examples include Lewmar, founded in the 50s, which designs and manufactures equipment for the leisure marine industry, i.e. yachts and speedboats. They were acquired by U.S. company Lippert Components earlier in mid August 2019, for around £30m. Older acquisitions tend to operate in less high-tech manufacturing sectors, such as Audley Builders Merchants, a manufacturer of building supplies. Founded in the early 70s and based on Anglesey, this company was acquired by a much larger, fellow Welsh building merchant Huws Gray in 2018.

So how do the differences in growth journeys look between high-growth companies that have IPOd versus those that have been acquired?

Discover the UK's most innovative companies.

Get access to unrivalled data on all the businesses you need to know about, so you can approach the right leads, at the right time.

Book a 40 minute demo to see all the key features of the Beauhurst platform, plus the depth and breadth of data available.

An associate will work with you to build a sophisticated search, returning a dynamic list of organisations matching your ideal client.