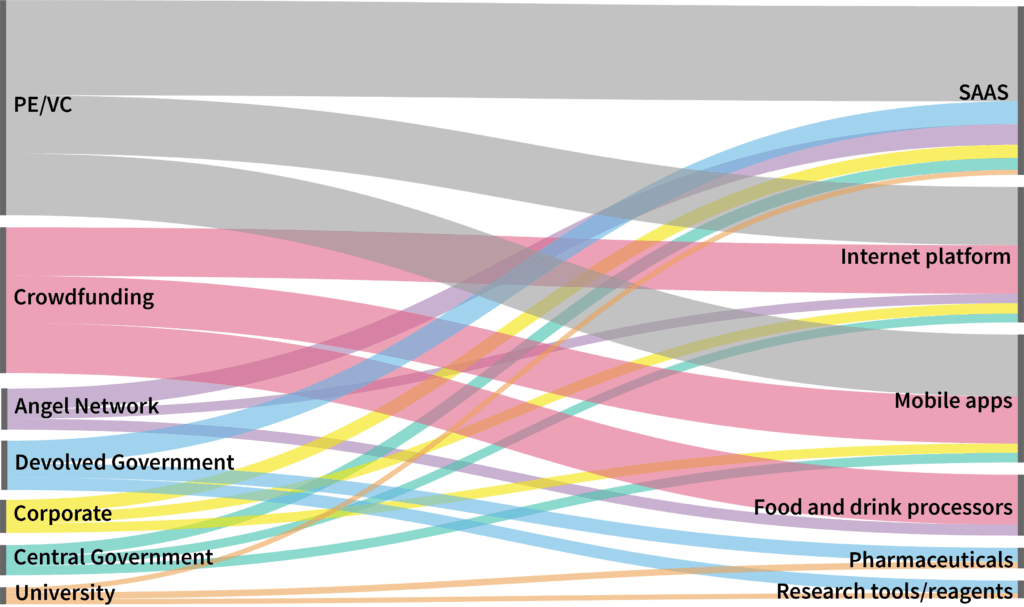

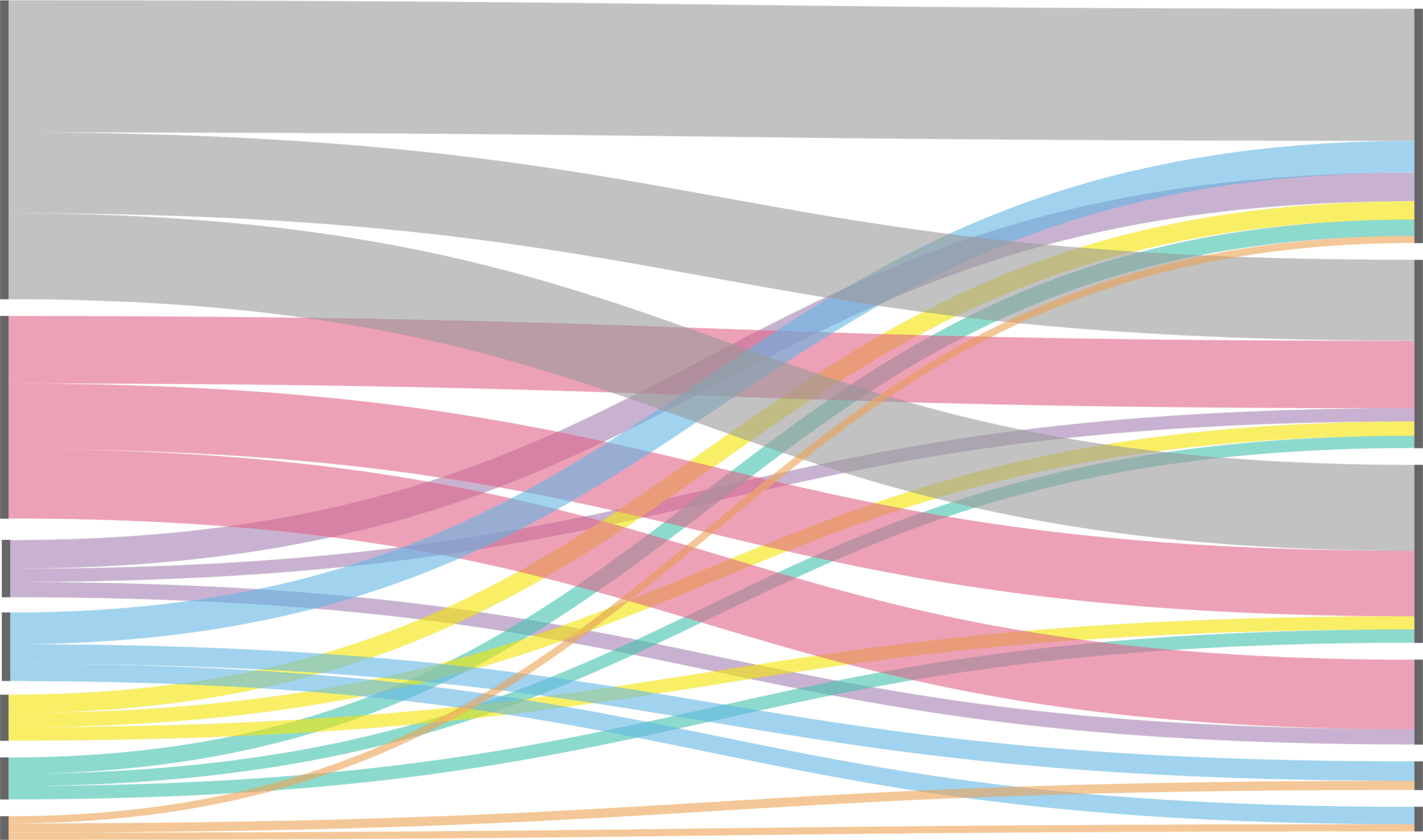

The UK is home to over 30,000 high growth companies, of many different shapes and sizes. To match this diversity, the country has many different types of investors offering a variety of funding options, expertise and support to young ambitious companies. This is the final part of our “investor type” blog series, with the first blog assessing the market share of these investors, and the second taking a more granular look at the average deal profile that they each are involved in. This third and final part takes a step back to look at where the equity is going, and into what sectors.

Geographically, we see an undeniable bias towards London, with 47% of all deals in 2018 secured by companies in the capital. The series of maps highlights the different regional strategies of investor types. Looking at the top sectors of each investor, we see certain strong sectors, such as Software-as-a-service, attract investment from all types of investors. University funds, more exclusive by nature, show slightly different sectoral preferences, primarily supporting companies in the medical and research sectors.