The Future of Blockchain Technology

Home » The Future of Blockchain Technology

Category: Uncategorized

In this post, we delve into the often misunderstood, yet undeniably revolutionary world of blockchain. Blockchain was first introduced anonymously in 2009, by someone under the alias ‘Satoshi Nakamoto’, following the release of their 2008 white paper (Bitcoin: A Peer-to-Peer Electronic Cash System). Since then, a plethora of blockchain startups have emerged that are using the technology to disrupt traditional industries like financial services, healthcare, and law.

To help explain the hype around this relatively new technology, we first outline what blockchain is exactly, and how the well-known Bitcoin blockchain operates. We then take a closer look at how some of the UK’s most innovative tech companies are applying blockchain solutions to real-world problems and business processes.

What is blockchain technology?

Essentially, blockchain is a digital ledger that records transactions securely, without the need for a regulatory authority. The word ‘blockchain’ aptly describes its function:

‘Block’

A ‘block’ is an online file which contains a group of transactions. Each block contains three main pieces of information. Firstly, it includes data about the transactions themselves, like their value, the date they took place, and the transaction participants. The number of transactions within a block varies, with one block on Bitcoin, for example, able to store up to 1mb of data, which can equate to several thousand transactions. Secondly, a block contains a unique code consisting of a series of letters and numbers—called a hash code—which is used to identify the block. Thirdly, a block contains the hash code of the previous block.

‘Chain’

The ‘chain’ element refers to the fact that each block is strung together in a chronological and linear arrangement. Perhaps the chain’s most important feature is that once a new block has been added to the chain, it cannot be undone. Any attempted change to the block will result in a new hash code being created, thus rendering a block immutable once added to the chain. This form of record-keeping ensures greater security from tampering, as the permanence of the block precludes hackers from removing or modifying it.

Features of blockchain

| Feature | Function |

|---|---|

Distributed Ledger |

Blockchain’s distributed ledger technology enables thousands of computer systems around the world to access and validate transactions. This sophisticated layer of verification provides a comprehensive and secure system of recording digital transactions. |

Decentralised System |

Transactions recorded on a blockchain only occur between transaction participants, without a central authority—such as a bank—required to facilitate them. This decentralised feature of the blockchain system means there are no fee-charging intermediaries involved, and hence no transaction costs. |

Immutability |

Once a block is added to a chain, it is immutable, meaning it cannot be removed or modified in any way. This shapes blockchain as an anti-corruption technology, with hackers unable to alter any transactions stored within blocks. |

The Bitcoin Blockchain

Blockchain was originally created to serve as a public ledger for cryptocurrency Bitcoin. The Bitcoin blockchain remains one of the most well-known and popular blockchains today.

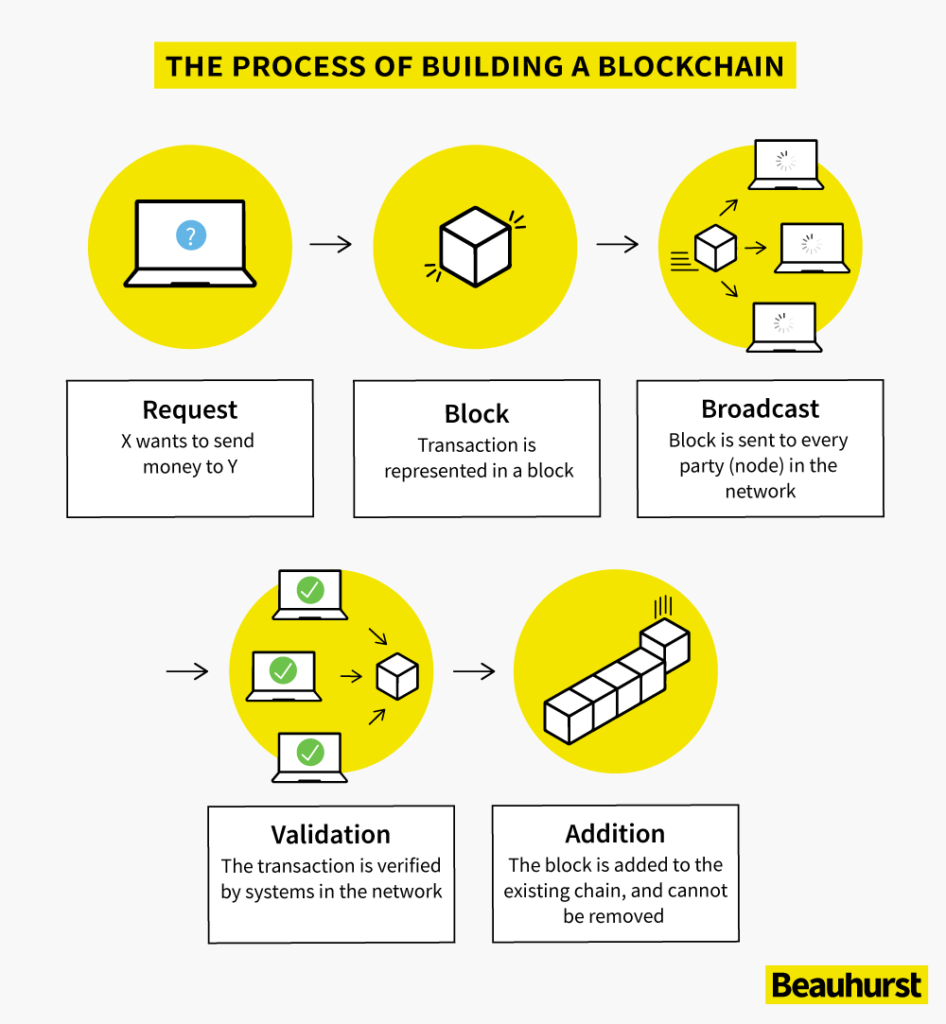

How does the Bitcoin blockchain operate?

Bitcoin uses blockchain as a platform to securely record transfers of the cryptocurrency from seller to buyer, without the need for a central bank. The process begins with a purchase request of Bitcoins. This transaction is represented within a block, which may also contain other similar transactions. Then, the block is broadcast to a network of computer systems, called ‘nodes’. Every party within the network must then validate the transactions. Upon validation, the block is permanently added to the chain, and cannot be removed or modified. The updated version of the blockchain will then be used.

What makes the Bitcoin blockchain secure?

In a blockchain, every block contains the hash code of the previous block. For a hacker to modify one transaction, they would subsequently need to modify every following block in the chain to ensure the hash codes remain consistent—a possibly never-ending task which makes blocks practically immutable. The use of blockchain technology for Bitcoin thus protects it from tampering.

The Proof-of-Work system is another way in which the Bitcoin blockchain boasts an ultra-secure system. Proof-of-Work requires ‘miner’ nodes to race to solve a complex computational problem, known as a hash function. This problem requires extremely large computing power, and hence expensive hardware systems, to complete, acting as a deterrent and barrier to malicious miners attacking the blockchain network. The race amongst miners to solve the problem also promotes efficiency in processing the transaction. The first miner to solve it is rewarded with newly-minted Bitcoins, providing incentives to process transactions as quickly as possible.

Industries disrupted by blockchain companies

Whilst Bitcoin is the most commonly used blockchain, blockchain technology can be adapted to record any type of digital information, and helps make supply chains more efficient and transparent. So it’s no wonder we’re starting to see blockchain adoption across a broad range of sectors in the high-growth ecosystem, from fintech and artificial intelligence to real estate technology, e-commerce, and the internet of things (IoT).

Blockchain is often referred to as a ‘disruptive’ technology due to the potential it has to transform industries as we know them today. Let’s explore how blockchain’s broad functionality could be used to disrupt the banking, legal and healthcare services, through a variety of different use cases.

Blockchain in banking and financial services

Blockchain banking offers a cheaper, quicker, and more secure payment alternative to traditional financial institutions. Blockchain banking would involve banks issuing their own digital currencies and distributed ledger systems for processing payments, similar to Bitcoin. As blockchain is decentralised, no middlemen service fees would be charged. This is particularly useful for cross-border financial transactions; with blockchain, overseas parties will save on both financial service fees and exchange rates.

With payments being processed as soon as they are verified, blockchain banking also offers a more efficient system. Bitcoin transactions, for instance, typically take 10 minutes to be verified by miners (at which point, the payment is immediately transferred, regardless of the parties’ locations). Additionally, due to blockchain’s immutable nature and its complex cryptographic-secured network, transactions are very secure. This secure payment channel offers unrivalled protection from hackers and thus enables payments to be highly safeguarded.

Blockchain in legal services

A large part of the legal services industry involves processing and storing sensitive information. This is high up on the list of possible blockchain applications, with digital ledgers functioning as a perfect tool for the sector.

Contracts

The legal services industry can tap into blockchain’s ability to securely store contracts through ‘smart contracts.’ A smart contract is a digital code mapped out on a blockchain, that automatically monitors and executes legal agreements. Smart contracts can be used when it’s possible to measure the triggering event of a contract digitally, such as when payments are made or public registries are updated. This automation eliminates the need for contractual monitoring by lawyers. Ethereum is a popular blockchain for facilitating smart contracts. The Ethereum blockchain platform even provides options for payment through blockchain, using its own cryptocurrency, Ether.

Conveyancing

Blockchain systems can also simplify conveyancing, where property is transferred from sellers to buyers. The conveyancing process involves many parties (buyers, sellers, both their legal representatives, and both their banks) and many documents (transfer of land contracts and certificates of title). Dealing with this number of documents and parties is often a lengthy and complex process. Instead, storing details of the property and relevant documents within a block, which can be accessed by all parties, would reduce correspondence between parties and requests for information, save time, and ensure confidentiality.

Blockchain in healthcare

The healthcare industry is dense with personal data records, medical insurance claims, and other pieces of important patient information, all stored in different systems. Blockchain infrastructure offers an easily shareable and secure system of patient management. This could operate through patient data being stored within a block. These digital assets can then be shared with different medical institutions and practitioners in real time, once the patient’s consent has been given.

Additionally, the use of blockchain technology in healthcare could create a more efficient and streamlined appointment process. Patients would not need to constantly provide their medical information every time they visit a new medical institution or practitioner, with their data readily accessible. This would also prevent the problem of data being lost and needing to be recollected, as in the case of missing blood test samples.

Discover the UK's most innovative companies.

Get access to unrivalled data on all the businesses you need to know about, so you can approach the right leads, at the right time.

Book a 40 minute demo to see all the key features of the Beauhurst platform, plus the depth and breadth of data available.

An associate will work with you to build a sophisticated search, returning a dynamic list of organisations matching your ideal client.

*This article was first published on 24th October 2019, and updated on 13th August 2020